2018年12月15日 星期六

2018年11月13日 星期二

2018年11月1日 星期四

Defending Radiation by Eating Salt

Defending Radiation by Eating Salt

Yesterday my friend, who is now an exchange student, spent one euro in printing his e-ticket at an Airbnb. He told me that he was taking Ryanair, the staff might not allow him to take the flight without the e-ticket, or paying ten euro in priniting the e-ticket at the airport. Finally, Ryanair did not require passenger to show their e-ticket on that flight. He was very happy as he told me that he was rational in economics sense. He told me that if he did not print the e-ticket at Airbnb and if he is required to show it, he might lose ten euro. The cost of priniting at Airbnb is smaller than expected codt of priniting at the airport.

This event leads me to think about the earthquake in Fukashima in 2011. Due to the earthquake, the nuclear power plant exploded. There was rumor that taking salt can prevent radiation absorbed into human bodies. As a result, demand for salt surged. Price of 100g salt even rose to $40 per 100g (normally it costs $5 for 100g unless you are buying luxurious salts). Many people claimed that the people rushed to buy salt were insane and brainless. However, was this really irrational?

Giving price of salt is $50, cost of curing cancer is infinity. Even if there were negligible probability that salts are useful, the expected cost saved is still much lower than you cost of a pack of salt. Due to the love towards family, many housewives rushed to buy salts in crowd and dirt markets. This action was completely rational.

At the end, my friend asked me, “Wilson, am I right? Am I smart?”. I replied, “You are right, however you are stupid.” He was angry and asked me if I were him, what would I do. And I told him, “I would of course print the e-ticket at school’s computer barn.”

Crimes and Interest Rate (Part 2)

Crimes and Interest Rate (Part 2)

I have collected the data of real interest rate and crimes rate in the US from year 1968 to 2014. Crimes rate is defined as number of crimes per 100,000 population, thus effect of population growth in crimes number is considered. Before looking at econometrics analysis, let first take a look of the correlation coefficient between interest rate and crimes rate.

Correlation coefficient between real interest rate to

Murder: 0.78

Rape: 0.37

Robbery: 0.17

Aggravated assault: -0.39

Burglary: 0.87

Larceny-theft: 0.70

Motor vehicle theft: 0.57

Data shows that there is a positive relation between real interest rate and crime rate. Moreover, the correlation between real interest rate and property crimes (the bottom three) is higher than the correlation between real interest rate and violent crimes (the top four). This shows that maybe impatient people just want to have earlier consumption rather than hurting others.

However, can we conclude that higher interest rate leads to higher crime rate? Surely no unless we can control the effect of all other variables that affecting crime rate, including GDP, unemployment rate, Gini coefficient, etc. Therefore, to investigate the casuality, we have to conduct sophisticated econometrics technique in order to isolate the effect of interest rate from all other variables.

I have calculated the first difference of interest rate and crime rate, and conducted the HP filter to the data. As a result, I can isolate the effect of the change in interest rate on change in crime rate. The followings are the effect of one percent increase in real interest rate of crime rate, parenthess is the t-statistics:

Murder: 2.46 (2.893)

Rape: 4.05 (3.695)

Robbery: 5.86 (6.271)

Aggravated assault: 3.00 (3.805)

Burglary: 4.01 (5.072)

Larceny-theft: 3.30 (5.043)

Motor vehicle theft: 1.85 (1.96)

The regression result shows that an increase in real interest rate will cause a higher crime rate, and the coefficients are all statistically significant. One percent increase in interest rate result in 2.46% increase in murder, 4.05% increase in rape, 5.86% increase in robbery, etc...

Therefore, data confirm that higher interest rate result in a higher crime rates.

2018年10月31日 星期三

Crimes and Interest Rate (Part 1)

Crimes and Interest Rate (Part 1)

Empirical findings show that crime rate and interest rate are positively related. In other words, when interest rate is higher, crime rate will also be higher. These two variables seem unrelated, this phenomenon, however, can be explained by economics.

Interest rate as a discount factor

“One dollar today worth more than one dollar tomorrow”. This sentence is right given a positive interest rate. If you have one dollar, you can invest and get back one plus the interest tomorrow. The higher the interest rate, the more you get, and the more valuable the one dollar today.

With the similar manner, what if you owe your friend one dollar? Should you repay it today or tomorrow? The answer is clear, you should postpone your repayment as you can get more interest if you postpone. The higher the interest rate, the less you have to repay.

Therefore, the existence interest rate adds value for today’s benefits and diluting future costs. The higher the interest rate, the more “impatient” the people are.

Crimes as an impatient act

When a person committ crimes, he/she gets the present enjoyment. For example, burglary and robbery let you get certain amount of money to spend now; assault allows you express anger to those you hate; rape… well….

Of course, after you get the enjoyment, you have to pay the cost. Yet, punishment will be made in the future. Since interest rate is a discount factor, your real cost will be lower when the interest rate is higher.

In part 2, we will dig into data to see whether higher interest rate leads to higher crime rate. A story will become a theory if it is verified by data.

2018年10月18日 星期四

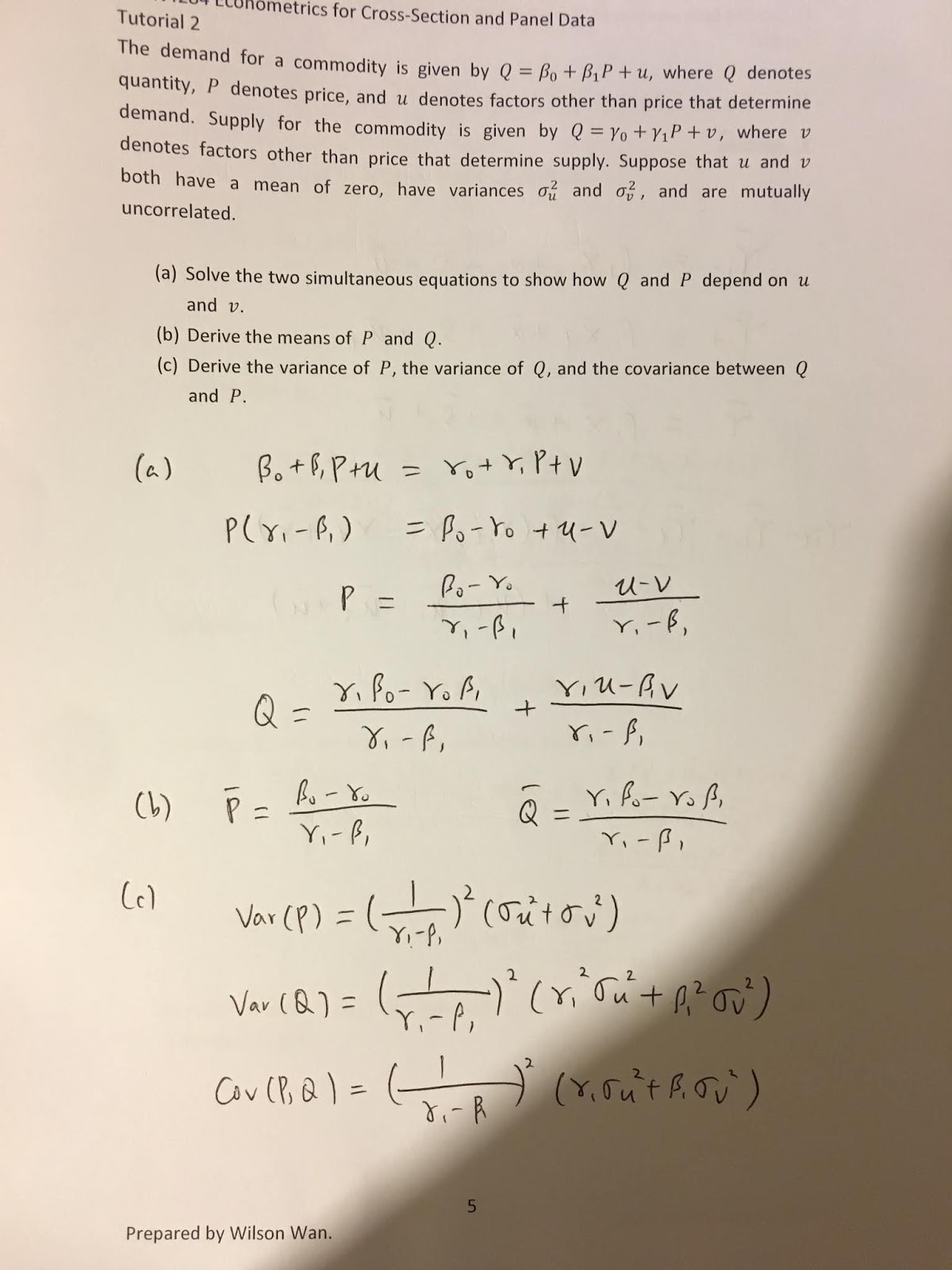

[ECON4284] Tutorial 2

Note:

https://www.file-upload.com/zmg0mqtzrolb

https://www.file-upload.com/zmg0mqtzrolb

For the last part, I dont know why I cannot upload the video. Just try to derive the answer by yourself. They are not hard.

2018年10月11日 星期四

Why Barbecue Mix Combo is More Costly than Barbecue Regular?

Why Barbecue Mix Combo is

More Costly than Barbecue Regular?

It is not uncommon to see that the price

of barbecue mix combo with rice/noodle is more expensive than barbecue regular

with rice/noodle. For instance, at HKUST LG1, barbecue pork with rice is $22

while barbecue pork mix soy sauce chicken with rice is $25. Many people tried

to use the concept of diminishing marginal benefit, diminishing marginal

utility or diminishing marginal use value, etc. to explain this phenomenon.

These explanations, however, have missed one crucial condition. In this

article, I will give a full explanation for the case that a combo is more

expensive than a solo.

The Condition of Diminishing Marginal

Utility

Many people use diminishing marginal

utility to explain this phenomenon. When a consume keep buying the certain

good, the additional utility (or benefit) will decrease. Picture that, what do

you feel for the first bite of your barbecue pork when you just finished the

8-hour lectures? You definitely feel very dim and very ecstasy. Then, what do

you feel when you are eating the tenth bowl of barbecue pork with rice? You will

think that they are shit. Therefore, if you have more variety of choices, the

diminishing marginal utility of each component is smaller. Thus, the aggregate

of your satisfaction is larger. As a result, you are willing to pay a higher

price. This is convincing, isn’t it?

The Missing Condition: The Combination Have

to be Complement

Well, if you tried to add some milk into a

cup lemon tea, I guess no one is willing to pay a higher price for this combo

than just a cup of lemon tea or just a cup of milk. The reason why the combo

can be sold at a higher price, or why consumers are willing to pay a higher

price for the combo, is that the combo are complementary to each other. Tofu is

complementary to roasted pork, thus consumers are willing to pay a higher price

for braised tofu with roast pork. Lemon tea and milk are not complementary to

each other. Consumers will not pay a higher price even if they exist

diminishing marginal utility.

2018年10月9日 星期二

如夢?如花?Adverse Selection and Online Dating

如夢?如花?Adverse Selection and Online Dating

Many people (in HKUST)

in the society nowadays find it difficult to find a girlfriend / boyfriend. As

a result, many of them resort to online dating in order to complete their

dream. Unfortunately, many people complain that the quality of their dating

partner is much lower than their expectation. Worse still, some unscrupulous

liars make use of the dating platform to scam people’s wealth. The reason

behind is that adverse selection is inherent in these types of dating

platforms.

What

is Adverse Selection?

Adverse Selection is one the

most crucial concepts in Economics. Professor George Akerlof introduced the

concept of Adverse Selection in 1970. The story is that due to asymmetric

information between buyers and sellers, buyers cannot distinguish the quality

of the products. Therefore, buyers will pay for the average price of the high

quality products and low quality products. Sellers of high quality products

will leave the market if the average price is lower than their cost. As a

result, only low quality products are left in the market. The low quality

products (which is called lemons) repel the high quality products (which is

called peaches).

Applications

of Adverse Selection

Adverse Selection can be found

in many cases. For example, in the insurance market, insurance companies cannot

distinguish between high-risk insures and low-risk insures. Therefore,

insurance companies will set the premium equals to their expected cost

(probably with a mark-up). In this case, the low-risk insures will think the

premium be too expensive and reject the offer. As a result, only high-risk

insurers will buy the insurance.

Another example is in the car

market. The buyers do not want whether the car is a peach or a lemon. Thus,

buyers will place the average price between a peach and a lemon when they are

offered a car. When this price is lower than the value of a peach seller, the

peach seller will leave the market. Eventually, only lemons are left in the

market.

Adverse

Selection in Online Dating

The adverse selection problem

is that many of the dating prospects are lemons. In other words, the quality of

clients tends to be lower than expected. You thought that your prospect is如夢, but eventually you meet up with 如花.

This is an inherent problem

due to asymmetric information. First, people are free to manipulate their

information at the online platforms. In order to achieve their goals (to get a

partner or to cheat money), the dating prospects would try to exaggerate their

types, such as claiming that they are 1.8meters high, having several

properties, making $50,000 per month, or even be able to swim to international

waters easily by just using single hand and battling with sharks, and blocking

hailstorm by single arm. Thus, quality is lower than expected.

Second, people participating

in online dating are the lemons in real life. If they are not the lemons, they

are able to find their partner in traditional way and do not need to rely on

online platforms. Therefore, only the losers and scammers would like to join

the online dating platforms.

How can the Adverse Selection

be mitigated? You might try to think about it and leave the comments.

2018年9月21日 星期五

2018年9月4日 星期二

2018年8月24日 星期五

Notice on Sat class

Hi students,

Sat class is cancelled due to my emergency issue, we will have the class on 29/8 (Wed) 8:30am. Please tell your friends I will not come on Sat.

Sat class is cancelled due to my emergency issue, we will have the class on 29/8 (Wed) 8:30am. Please tell your friends I will not come on Sat.

2018年8月21日 星期二

Notice for sat class students

I will finish Ch.9 at this Sat (25/8). Please come on time. I will try my best to finish before 10:30am. In case if we cannot finish at 10:30, we will extend the class until we have done.

Please review today’s materials.

Please review today’s materials.

2018年8月20日 星期一

Update of class schedule

For Monday and Tuesday class students, we have completed the micro syllabus. There are no classes for remaining week. We will resume macro at Sept.

2018年8月13日 星期一

靠信用卡零成本搵錢

(為左令大家更容易理解今次搵錢機會,本文將會用口語)

之前提及到大家應該多用信用卡消費,因為可以係消費既同事儲番多少積分,積少成多換曬d現金回贈或者禮券。

今次介紹一張信用卡比大家,Citibank Rewards Visa Card。首先講下呢張卡既特別之處,然後再教大家點樣零成本搵錢。

大家可以憑住Citibank Rewards Card係超級市場、電訊公司、百貨公司每消費$1得到5分(如果係生日月入消費仲會有8分),每25000分可以換到$100現金回贈(2%回贈率),亦可以用22500分換$100惠康禮券(2.8%回贈率)。如果惠康券係岩用既,變相每期交電話費,或者每月定時定後去百佳惠康入貨(記得儲埋易賞錢同埋八達通日日賞),都可以慳番2.8%。

同時我都知有好多人想儲飛行里數,呢張卡亦岩曬你。呢張卡每15分換到1Asia Miles,姐係係超級市場、電訊公司同百貨公司既消費會做到$3一里,儲夠15000里就換到台灣既機票、20000里就去到日本,都咪話唔吸引。

之後講下呢篇文既重點,點樣零成本搵錢。最近Citibank搞左個Member gets members 既活動,如果有人介紹你申請張卡,就可以即刻拎到$100回贈,簽滿頭$10000亦有135000分送。換言之,假設我申請到張卡,買$10000惠康券,我會得到50000基本積分同135000迎新積分,185000分可以換到$800惠康券。咁姐係用$10000買到$10800惠康券,然後可以95折賣番d券出去,你會得到$10260,咁就剩袋$260了。

如果你想要飛行里數,頭$10000,我當你唔中果3類消費,計埋迎新你都會有145000分數,姐係換到9666里,計番係$1.035就有一里。市面上好多卡平均都要$4-$6一里,$1.035換到一里實在抵到爛。

所以,大家不妨搵下身邊有無人推薦你。如果無既,歡迎拉落我個blog最底,會有條Citibank既link,記得申請果陣入番我既Reference Code,咁就可以搵到d免費錢。就算你覺得煩唔想買賣,直接申請都有$100送,免費既錢唔係唔要掛?

Citibank Credit Cards (Earning HK$100)

Referral code: C002571236

https://www.citibank.com.hk/global_docs/chinese/credit-cards/mgm/promotion-mgm-referee.html

Citibank Credit Cards (Earning HK$100)

Referral code: C002571236

https://www.citibank.com.hk/global_docs/chinese/credit-cards/mgm/promotion-mgm-referee.html

2018年8月12日 星期日

理財隨筆(13)—開源(七)續

分段入市法

分段入市法即把計概購買股票的金錢,分開不同時間或價位購入。例如你打算把$60000投入一隻股票,你可以每兩、三個月投放$20000,投放三次;或先把$20000投放一注,每當股價跌10-15%再下一注,再跌10-15%下最後一注。分段入市的方式可拉低成本。

讓我利用一個簡單的例子來解釋這個方法。例設你只作一次性的投資,股票在短期內或升或跌,你的購入價高於平均或低於平均的機會率是均等的。但若你利用分段入市法,假設股價在三段時期為$5、$10、$15,而你每個時期也會購入$1500的金錢,三段時間你將購入300、150、100股,即代表你用了$4500購入550股,平均每股只是$8.18。三段時間之中,有兩段時間股價比平均價高,利用分段入市便能拉低投資成本了。

月供股票計劃

月供股票計劃即每個月投放相同的金錢於某隻股票,是分段入市的一種,亦有拉抵成本的作用。月供股票的好處是入場費低,在香港股票市場,投資者只能以一手為單位,而大部份優質股票,每一手也需用上數萬元,月供股票便能夠讓投資者,以較低的入場費,慢慢累積優質股票。只要時間夠長,月供股票是資產增值的好方法。

市面上很多銀行及證券行也提供月供股票服務,大家必須先了解清楚收費詳情,才進行買賣,否則,高昂的交易費用會吃掉大量投資回報。

2018年8月11日 星期六

理財隨筆(12)—開源(七)

(3) 買入股票的方法

著名投資者茫格曾說:「買入甚麼比甚麼時候買入更為重要。」這句說話的意思是,若你購買的是優質股,不論你在那一個價位買入,只要長期持有,終會得到利潤。這是絕對正確的,假如你購入的是垃圾股,不論你購入的股價是一年低位、三年低位,甚至是上市以來最低點,企業的價值一直下跌,股價只會繼續創新低;相反,就算你在歷史高位購入優質股,由於企業價值會一直上升,所以股價將會繼續穩步上揚。當你一直持有優質股票,你的財富將會持續增值。

長遠來說,股價反映企業的價值;但短期來說,股價受著市場氣氛需求供求影響,會有一定程度上的波動。雖然只要是購入優質股票,股價長遠來說會上升,但是假如能夠利用便宜的價錢購入,回報率會更為可觀。問題是,世界上沒有人知道股價明天會升還是跌,捕捉最低股是極其困難的。以下我將會介紹一些方法,盡量拉底買入價,增加投資股票的值搏率。

2018年8月10日 星期五

理財隨筆(11)—開源(六)

優質股是大型、已發展成熟的企業,它們都有穩健而穩步上揚的業務。

大家別以為股票是很複雜的投資工具,優質股是很容易在日常生活中找到的。由於優質股是已經成熟的大企業,擁有一定數目的顧客群,而你很大機會是其中之一。所以,你能夠在日常生活中,找到不少優質股。

舉個例子,在日常生活中的衣食住行已經能夠找出大量優質股。在衣之中,深受女性市場歡迎的莎莎集團、內地市場喜歡的六福集團、周大福;在食之中,每天早、午、晚市都坐滿人的大快活、大家樂;在住之中,有受惠於樓價上升的地產股及房托股,如新鴻基地產、恒基地產、領展,亦有日常生活需要的煤氣、電力;在行之中,有壟斷的港鐵公司。這些所有都是擁有大量客源,而且業務蒸蒸日上,投資優質股有穩中求勝的效果。

收息股是已成熟的企業,它們已經擁有完善的收入來源,不會再冒險尋求擴展,所以風險是最低的。

由於收息股不會再尋求擴展,升值潛力是很低的。但它們擁有以上兩類股票沒有的優勢,就是派息能力。大部分潛力股是派很少息,甚至不派息的,它們普遍會保留資金,作繼續發展之用;優質股相對派息較高,但它們仍有發展需要;而收息股不需保留資金,故大多會把盈利全部派出。

這裡大家要留意的,當股票派息後,股價會自動調整。例給股票派發$1股息,股價會自動下跌$1,故此盲目追求高息股是沒意義的。

由於收息股風險低、潛力低,投資收息股應該是人生中後期的選擇。年輕是應該先投資潛力股及收息股,待資產增值,漸大時換取收息股,得到永續的收入。

2018年8月9日 星期四

理財隨筆 特別篇

最近港鐵建築工程的事滿城風雨,醜聞一個接一個爆,在這裡我們談談港鐵公司這隻股票。大家可能以為,港鐵的營運模式只是收取乘客車資,提供運輸服務,這未免太簡單了。無論是收入申盈利能力或是成本控制,港鐵公司都是非常優秀的。

首先,港鐵擁有多元化的收入來源。除了香港的鐵路營運,港鐵公司的業務幅蓋中國內地、英國、澳洲,未來亦將發展北歐地區的鐵路營運業務,持續的全球鐵路網絡發展將為港鐵帶來穩步上揚的收入。

其次,港鐵亦利用本身的優勢帶來巨大收入。除了鐵路運輸,港鐵亦不斷在鐵路站上蓋進行物業投資,包括住宅樓宇及商場寫字樓。住宅樓宇用作於銷售,例如位於大圍站上蓋的名城、車公廟站的溱岸,都是中等至高收入人士的住宅用地;而商場及寫字樓則用作出租,例如九龍灣德福商場、青衣的青衣城,商場數目亦不斷發展,如青衣成2期及將會推出的大圍商場。香港地少人多,地價只會不斷向上,擁有優質地段的港鐵因此擁有巨大的優勢。

在控制成本方面,由於鐵路網絡對社會發展極其重要,發生事故時政府會「包底」,大家應該知道數年前,政府使用了大量金錢補貼港鐵在沙中線工程延誤的損失。加上港鐵可加可減機制給予港鐵把成本轉介予消費者及政府的能力。所以,港鐵公司虧損的可能性極低。在有多元化收入及成本控制能力之下,港鐵公司是一間非常優質的企業。

最近港鐵不斷爆出醜聞,但這些對港鐵的收入完全沒有影響,物業投資將會繼續帶來收入,消費者亦會繼續使用港鐵,總總蹟象顯示,港鐵的優質情度沒有下降。短期股價會受到投資者情緒影響,會有股價下跌的現象,股價下跌卻是一個投資的好機會,大家在這段時間不妨留意一下。

本人持有港鐵公司股票,仍會繼續買入。

2018年8月8日 星期三

理財隨筆(10)—開源(五)

(2) 建立一個股票組合

在眾多投資產品之中,我最推薦的是股票。

首先,大家必須明白一個概念。炒股是賭博,並不是投資。股票不只是冰冷的數字,而是一個活生生的企業。股票,英文是Share,即是一部分的意思,買股票,便是購買了公司的一部分。當企業有利潤時,你們會得到你買的那部分的利潤,當企業一直得到盈利,你便能一直分得利潤。所以,購買股票能為你帶來連綿不絕的收入,是一種資產。

當你明白「買股票便是買企業」的時候,你便會明白買股票前,對企業作出分析的重要性。你希望分享盈利,你必須購買有盈利能力的股票。市場上充滿沒有盈利能力的「垃圾股」,甚至是只為得到投資者金錢的「老千股」,這次股票在經過對企業分析後,是完全能夠避開的。

好的股票可分為潛力股、優質股和派息股。故名思義,潛力股是在將來有巨大升值潛力的股票,風險亦會較高。大家可以想像一下,未來十年、二十年、甚至三十年後,那一個行業會漸漸壯大起來?科技、保險、醫藥、環保、電動車等等。這些都相信是未來的經濟推動力,所以相應的股票如騰訊、平保、友邦、比亞迪等,便擁有潛力股的特徵了。

當然,世上沒有人會知道未來是怎樣的。所以潛力股的風險較大,大家不能過度集中投資於潛力股。

2018年8月7日 星期二

理財隨筆(9)—開源(四)

建立資產是開源的最重要部分,因為它是決定你能否達至財務自由的決定因素。

資產是一種能為你一直帶來收入的物件,最簡單的資源是銀行存款,銀行存款能夠為你帶來利息收入,而這種收入是被動的。只要你的被動收入大於支出,你便達至財務自由的境界。那時候,是金錢為你工作,而不是你工作為了金錢。以下是幾種建立資產的方法。

(1)設立一個投資組合

市場上有不少投資工具,包括物業、債券、股票、基金、保險年金等等。每一種投資各有優劣,投資前必須先了解產品特性。

物業投資是購買物業擁有權後,擺放著並等待物業價值升值,或把物業出租,獲取租金收入。

債券是一種借貸。當你購買公司發出的債券,即代表你把一部分金錢借給對方,而對方需定期歸還利息及歸還本金。

股票代表公司的價值。你購買了股票,就表示你成為公司的部分擁有者。當公司有盈利時,你有權分享公司的利潤。

基金是一個組合,組合內或許是多隻股票、多隻債券、或股票加債券。

保險年金是在一定時間內進行特定供款,經過一段時間後,定期給投資者一定的收入。

大家應根據自己的風險承擔能力,選擇自己的投資組合。物業、股票的風險較高,但回報很高;基金、債券風險較少,回報亦較少;保險年金、定期存款風險低,但回報亦低。雖然每個人有不同的喜好,但我會建議大定採取「先增值,後現金流」的方式,年輕沒有負擔時,先投資於高風險的股票上,年紀漸大時便一步步把組合投資在低風險的產品之中。

2018年8月6日 星期一

理財隨筆(8)—開源(三)

(2) 利用「步行」賺錢

上一章提及利用額外工作而獲得額外金錢,相信大部分人都不太喜歡吧。但賺錢從來不是容易的事,你要明白一個概念,每一分一毫都得來不易,這樣你才能把你每一分每一毫發揮最大用途。這一章,我會介紹如何利用「零付出」賺錢。

以下兩個Apps,便讓你在日常生活步行之中賺到一點點金錢,sweatcoins 及 lifecoins。這兩個apps會自動把步行數字轉換成它們的虛擬貨幣,而它們的虛擬貨幣是可以進行交易的,而它們的虛擬貨幣能夠在部分歐美國家的商舖使用,所以它們會有一定的價值。每天你或是上班、或是上學,都需要走路。這兩個apps便能把步數自動轉成虛擬貨幣,你額外付出的力是零!

下載過程是最麻煩的。由於sweatcoins 及 lifecoins 沒有在香港apps store上架,所以只能先把apps store位置轉為英國或美國,下載後轉會香港,如何改善位置請自行google吧。賺取的虛擬貨幣如何賣呢?同樣google能夠幫助你,尋找sweatcoins trading 或 lifecoins trading 便能找到不少買家了。

轉換app store 位置後可以用我下面的link下載兩個apps.

每天回報是很少的,但你付出了甚麼呢?零付出得到正回報,回報率是ERROR!

2018年8月5日 星期日

理財隨筆(7)—開源(二)

(1) 番part time

找兼職工作是增加收入的最直接方法。或者你會說,每天朝九晚七已經很累了,如果再工作呢?這是對的,工作是很苦,但正如我上一章說過,早一天找到初期資金進行投資,你才能早一歲達至財務自由,能夠真正享受生活。而且,當你漸漸老去的時候,你會發現想努力已經力不從心了。

假如你是平日朝九晚六的工作者,周末便是做兼職的好時間。例如:你可以利用你的知識,替中小學生補習。現今社會對補習的需求是很大的,時薪$150-$200的補習工作不難找到,假如你在周末能替學生補習6小時,一個月便能得到$3600-$4800額外收入。很小嗎?別忘了,今天每月$4500,可是十年後的一百三十萬元。

除了周末的時間,你亦可以善用放工後的晚飯時間。近年愈來愈流行的外賣平台亦為我們獲得額外賺錢的機會。外賣平台是餐廳把外賣外判的方法,外賣平台如Uber Eats, Deliveroo, Food Panda, Honestbee 等等,當顧客在它們的平台點餐,它們便會尋找附近的外賣員運送外賣,外賣員能以駕車或步行方式上班,工資則以送餐次數計算,多勞多得。所以,你可以嘗試在放工後,擔任送餐員,送兩至三餐便可以把當天的飲食費用及交通費用賺回來了。我的網頁下有外賣平台Uber Eats的登記連結,大家坐言起行的話可以在那裡登記,完成一定送餐數字會有額外回贈的。

2018年8月4日 星期六

理財隨筆(6)—開源(一)

開源就是要增加自己的收入。很多人會覺得,無論怎樣儲蓄,例如每月儲起$4000,十年也只是多了$480,000,沒有甚麼作為,倒不如拿來消費,得到即時的快樂。所以,我必須在討論開源的方法前,首先談談開源的重要性。

假如你只把儲蓄放進月餅罐內,十年後的確只會有$480000。但如果你能夠進行投資,十年後又會變成怎樣呢?

假設投資年回報率為15%,每月投資$4000將會有以下效果。

第一年年尾:$51,441

第二年年尾:$111,152

第三年年尾:$180,462

第四年年尾:$260,913

第五年年尾:$354,298

第六年年尾:$462,295

第七年年尾:$588,516

第八年年尾:$734,564

第九年年尾:$904,090

第十年年尾:$1,100,868

假如你能夠每月把儲下來的$4000,投資在年回報15%的投資工具,十年後的你便成一位「百萬富翁」了。年回報15%的投資工具容易找到嗎?追蹤恒生指數的盈富基金(2800)歷史平均表現就有每年15%回報率了。

現在,你還會覺得節省下來的數百至一千多元沒意思嗎?假如你把每個月節省下來的$1000投資滾存下去,加上每月的$4000,十年後你會有$1,376,086,這是$275,217的差距嗎?非也!假設你有置業目標,或許你要進行按揭貸款,假設你進行八成按揭(即付20%作為首期),$275,217能助你借得$1,376,085,你置業的預算增加了超過一百萬元。

假如你能夠投資的資金愈大,或投資年期更長,你的回報將會變得更豐厚。所以,在下一章開始,我會談談增加收入的方法。現在,你還在胡亂花錢,打算遲一些才儲蓄投資嗎?做與不做當然是你的決定,將來市場會給你你今天選擇的成果。十年後,沒有人知道世界會變成怎樣,但你有能力在今天為自己的十年後建立更好的生活。

2018年8月3日 星期五

理財隨筆(5)—儲蓄(四)

(2) 成為各大集團會員

不少大集團商戶也推出會員計劃,當消費者於他們的商品消費時,出示該集團的會員卡,便能夠獲得相應積分,而當積分累積到一定數目,便能夠換取折扣優惠。例如於百佳集團、屈臣氏、豐澤購物,可以累積「易賞錢」積分,回贈計大約是0.2-0.4%;於惠康集團、中原則可以累積「八達通日日賞」,回贈率大約0.5%。

其他類型的便利店亦有會員計劃,例如7-11的7-Fans、OK便利店的OK齊齊印、mannings的mannings會員卡、日本城的JHC。飲食方面,大家樂、吉野家、麥當勞、KFC等商戶亦有會員計劃,在該商戶消費時亦能得到折扣優惠。

現今科投發達,只要有一台智能手機,便能把各商戶的電子會員卡存放於手提電話內,不需為帶卡而煩惱。

(3) 使用電子錢包消費

電子錢包消費是信用卡消費的一種,其運作模式是透過流動支付工具,如手提電話,把已登記的信用卡進行扣帳進行購物。除了能累積信用卡積分,電子錢包公司亦經常提供折扣優惠。常見的電子錢包包扣PayMe、支付寶HK、微訊支付,它們在指定消費均有特定折扣。

把八達通開通自動增值功能亦是一種節流的方法。八達通餘額達到負數時,八達通公司會自動把你已登記的信用卡扣帳。這樣就代表你每一次消費,已經能夠得到相能的信用卡消費回贈。

假如能善用以上方法,就算每天只能節省一點點金錢,以月或年來算,其數目亦是不少的。但要注意的是,千萬不能過度消費。假如你是沒有自制能力的人,使用現金消費才是最好選擇。

2018年8月2日 星期四

理財隨筆(4)—儲蓄(三)

在介紹各種能夠節流的工具前,我希望為大家介紹一個概念「莫因害少而為之,莫因利少而不為。」這裡的「害」,是指你各種不必要的支出,例如喝名牌咖啡、穿名貴波鞋、選擇方便而較為昂貴的交通公具等等。而這裡的「利」,便是能夠節省下來的一分一毫。即使是一分一毫,你也不能忽略它。

(1) 使用信用卡消費

信用卡是一把雙面刃,不當試用會變成過度消費,理財不善遲還款項,更會面臨「罰息」,但如果能善用信用卡,它絕對能讓你節省大量金錢。

信用卡不單只是有先消費,後結賬的作用。不同信用卡擁有不同的特性,部分是現金回贈、部分是儲積分兌換禮物、部分是累積飛行里數。假如你有自制能力,不會因為擁有信用卡而過度消費,使用信用卡絕對是百利而無一害。試舉一個例子,部分信用卡是每消費$200,便有$1回贈(0.5%回贈率)。假設你每月消費$8000,使用信用卡消費便能為你節省$40。除了$40信用卡回贈,假如你把延遲付出的$8000存放在有1%年利率的存款戶口,你將會再得到$7利息。$47是很少的數目嗎?是的,但別因利少而不為,省下來的,經過投資,將會為你帶來豐厚回報。

坐言起行吧!申請你人生中第一張信用卡。在我個人網頁最底部,有不少推薦的信用卡,大部分申請要求不高,回贈率平均也有1%以上。套用於以上數字,每個月便能省下$87,每年省下超過$1000了。

2018年8月1日 星期三

理財隨筆(3)—儲蓄(二)

真正有效的儲蓄,並不是在月尾收入減去消費的數字。假如你一直以來都是這樣想的,相信到月尾時,你總是把錢都花光吧。真正有效的儲蓄,是在你得到收入的第一天,把一部分抽出來,存放在一個地方,而只能消費剩下的部分,不論發生任何事,絕對不能拿儲蓄的部分出來消費。

所以,有效的儲蓄是 收入-儲蓄=消費 , 而不是收入-消費=儲蓄。

明白這個概念後,你地做的是了解自己的消費習慣。你可以嘗試利用各種Apps去紀錄自己每天的支出,月尾是便能夠了解自己的消費模式,找出甚麼消費是不需要的。其中一個我推薦使用的是「樂享退休GPS」(https://mpfa-retirementapps.com/referral?code=jGjwF0FmTHGX),這個App能讓你紀錄每天支出,在紀錄的同時,亦能夠儲積分換禮物。

下一章,將會介紹其他造到節流的工具。

2018年7月31日 星期二

理財隨筆(2)—儲蓄(一)

儲蓄(一)

要達至財務自由,方法是開源及節流。這裡我先談談節流。

假如我跟你建議,把30%的收入儲起來,你可能會跟我說:「我月入才一萬多,每月儲起$4000-$5000,一年才$60000,十年才$600000,$600000有什麼作用呢?能買樓嗎?既然買不了樓,倒不如花了它。」這是一個十分錯誤的看法,六十萬元的確不足夠買樓,儲蓄是隨年漸長的,你第一年的工資是每月$15000,十年後不會也只有$15000,你的儲蓄數字必須隨著收入上升既增加。而且儲蓄只時第一步,不造出第一步,後面的文章也不需要看了。

節流,即是要減少支出。換言之,這亦代表增加儲蓄。網絡上流傳著很多儲蓄方法,假如你在搜尋器搜尋「如何儲蓄?」,你將會找到海量的搜尋結果。但大部分儲蓄方法,都標榜著「簡單、方便、輕鬆」等等。我不是說這些方法必定沒有用,但我希望各位明白一種道理,你必須付出一直程度的努力,少可以造到最有效的儲蓄能力。

從今天起開始吧,無論你是每月只有$2000零用錢的學生、還是月入三萬的工作人士,假如你沒有儲蓄習慣,希望你可以嘗試,每月儲蓄最少30%,你的人生將會變得不一樣。

下一章我會介紹如何有效地助你達成儲蓄目標。

2018年7月30日 星期一

理財隨筆(1)—不可能的任務

不可能的任務

相信有不少年輕人經常聽到老一輩的人說:「後生仔,讀好啲書,大學畢業搵一份安安穩穩既工,將來先至會發達!」但是,一份安穩的工作真的能夠在現今社會致富嗎?試想想,假設你能夠成功大學畢業,並找到一份月入$15,000的工作,每年加薪10%,是不錯嗎?來做一些計算,第二年月薪是$16,500,第三年是$18,150等等⋯⋯到了第五年,你的月薪才是$21,962,即年薪是大約二十六萬元。五年過去了,假設你不吃不喝、沒有支出、甚至不需交稅,你一年只能造到二十六萬元的儲蓄,這樣的步伐能使你致富,能夠使你財務自由嗎?答案是或許可以的,但時間必然很慢長。

以上例子還有一個不切實際的假設,人生是不能沒有支出的。工作時給予父母的家用、日常生活的必要支出、甚至娛樂開支,總總都需要用上金錢。再加上生活在香港的我們,還要負擔買樓的壓力;再加上建立家庭的壓力,這些所有所有,都是關乎一個命題—你有沒有錢?考慮到以上巨大的支出,單憑一份安穩的工作,是不能夠使你致富的。這系列文章的作用,就是一步步指導你,協助你如何更有效、更容易地登上致富之路,成就你當初認為是不可能的任務。

2018年7月29日 星期日

[IB HL Econ] Aloca's natural monopoly

Since the production of aluminum is capital intensive, it is subject to large economies of scale. The production of aluminum is intensive in energy, as smelting requires a lot of electricity. Also it is intensive in raw materials (bauxite). Therefore, Alcoa (The Aluminum Company of America) controlled quickly the procurement of these crucial inputs. Signing up for hydroelectric power before construction and managed to stake out all the best sources of North American bauxite for itself.

The efficiency gains made entry more difficult and protected its leadership.

The efficiency gains made entry more difficult and protected its leadership.

2018年7月25日 星期三

2018年7月23日 星期一

2018年7月22日 星期日

Updated schedule for all classes

Class A (Mon and Thurs)

12/7, 16/7, 19/7, 23/7, 26/7, 20/8, 23/8, 27/8

Class B (Tue and Fri)

13/7, 17/7, 20/7, 24/7, 27/7, 21/8, 24/8, 28/8

Class C (Wed and Sat)

23/6, 7/7, 14/7, 18/7, 21/7, 25/7, 28/7, 18/8, 22/8, 25/8, 29/8

12/7, 16/7, 19/7, 23/7, 26/7, 20/8, 23/8, 27/8

Class B (Tue and Fri)

13/7, 17/7, 20/7, 24/7, 27/7, 21/8, 24/8, 28/8

Class C (Wed and Sat)

23/6, 7/7, 14/7, 18/7, 21/7, 25/7, 28/7, 18/8, 22/8, 25/8, 29/8

2018年7月21日 星期六

2018年7月18日 星期三

2018年7月17日 星期二

2018年7月16日 星期一

2018年7月15日 星期日

2018年7月13日 星期五

Tentative schedule for econ classes

Class A: Sat and Wed

12 classes (8:30am-10:30am)

23/6, 7/7, 14/7, 18/7, 21/7, 25/7, 28/7, 15/8, 18/8, 22/8, 25/8, 28/8

Class B and C: Scheduled

12 classes (8:30am-10:30am)

23/6, 7/7, 14/7, 18/7, 21/7, 25/7, 28/7, 15/8, 18/8, 22/8, 25/8, 28/8

Class B and C: Scheduled

2018年7月6日 星期五

2018年6月26日 星期二

2018年6月22日 星期五

訂閱:

文章 (Atom)